Financial Due Diligence in M&A: What Every Tech Founder Needs to Know

Financial Due Diligence in M&A for Tech Founders Guide

Financial due diligence is the most rigorous and consequential phase of any M&A transaction. For tech founders, it is the moment when every assumption buyers have made about your business is tested against the reality of your books. Understanding what due diligence in m&a transactions involves, what buyers look for, and how to prepare your financials will help you navigate this phase with confidence and protect the value you have built.

Key Takeaways

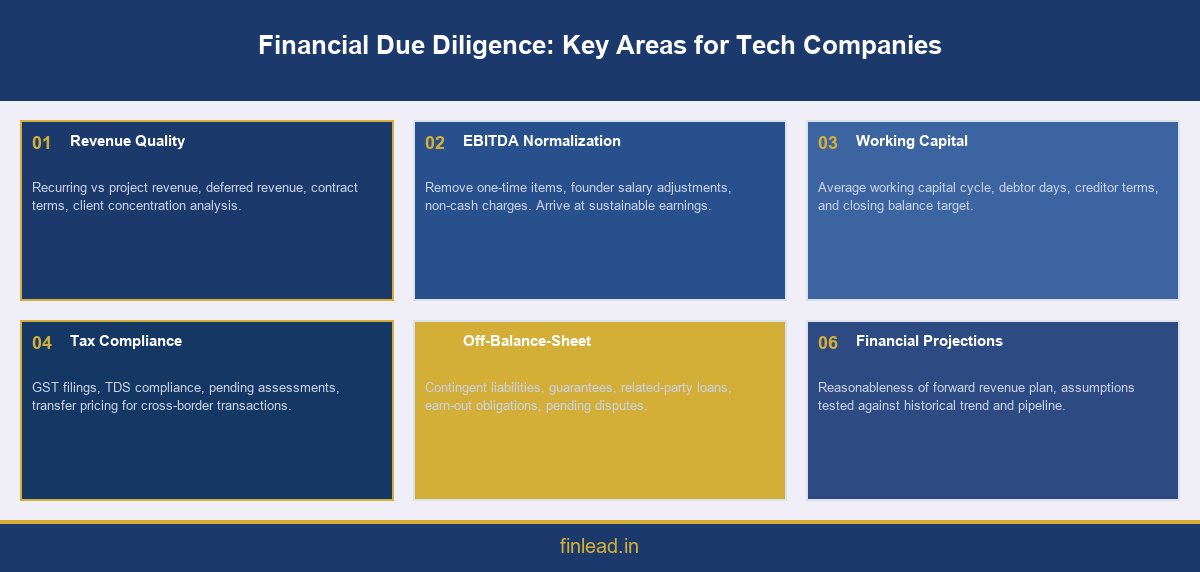

· Financial due diligence examines revenue quality, EBITDA normalization, working capital, and off-balance-sheet risks.

· Buyers will restate your financials independently and use their findings to negotiate price or deal structure.

· Preparation and transparency in financial due diligence reduce deal risk and protect your valuation.

What Financial Due Diligence Covers in an M&A Transaction

Financial due diligence in M&A transactions is a structured review of a company's historical and projected financials conducted by the buyer's accountants, typically from a Big 4 or mid-tier firm. The goal is to verify the accuracy of the financial information presented in the CIM, identify any risks or adjustments that affect valuation, and provide the buyer with a basis for the final purchase price.

For technology companies, the review typically covers: three years of audited financial statements plus the current year's management accounts; a detailed revenue analysis broken down by client, service type, and contract structure; EBITDA normalization to remove one-time items and founder-related adjustments; working capital analysis; and an assessment of net debt and cash positions at closing.

FinLead supports sellers through the full financial due diligence process as part of its M&A transaction services.

Key Financial Documents Buyers Will Request

The list of documents requested during financial due diligence can seem overwhelming, but it follows a consistent pattern. You should prepare and organize the following before entering any sale process: audited annual accounts for the past three years; monthly management accounts for the current year and prior year; revenue schedule by client, invoice, and contract period; payroll and headcount schedules; fixed asset register; details of all related-party transactions; and bank statements for the past 12 months.

For companies with international clients or operations, additional documentation will be required for transfer pricing, GST treatment on cross-border invoices, and TDS compliance. Having these organized in advance demonstrates financial discipline and speeds up the review considerably.

Red Flags That Delay or Kill Deals

Several financial findings consistently cause deal complications or price reductions. Revenue recognition issues top the list. If revenue is being recognized before delivery is complete, or if deferred revenue balances are understated, buyers will apply aggressive adjustments. Similarly, if large advance payments from clients are not properly reflected as liabilities, the working capital adjustment at closing can materially reduce the net proceeds to the seller.

Related-party transactions at non-market rates, undisclosed loans from the company to the founder, contingent liabilities not reflected in the accounts, and underprovided tax exposures are all findings that trigger renegotiation or price reductions. Conducting a thorough internal financial review 12 months before a sale, ideally with the support of your M&A advisor, allows you to identify and resolve these issues before buyers find them.

Review how FinLead has handled complex financial due diligence scenarios in past transactions.

How to Prepare Your Financials for Due Diligence

The single most important preparation step is to ensure you have audited financials for at least the past two to three years. Buyers are highly skeptical of management accounts that have not been independently verified. If your accounts have historically been compiled for tax purposes only, consider upgrading to a full audit before entering the market.

Prepare a normalized EBITDA schedule yourself, showing clearly the adjustments you are making and the rationale for each. This demonstrates commercial awareness and reduces the gap between your view of the business and the buyer's initial assessment. Include a clear explanation of any one-time items, founder remuneration adjustments, and non-cash charges such as depreciation and amortization.

Work with your CFO or finance team to produce a clean working capital schedule showing the average working capital required to run the business through the year. Buyers will negotiate a working capital target at closing, and having a well-supported number in advance reduces the risk of a last-minute dispute.

To prepare your financials with expert support ahead of a sale process, speak with FinLead's advisory team.

Conclusion

Financial due diligence in M&A transactions is not something that can be improvised. It is a structured, evidence-based review that tests every claim you have made about your business. Tech founders who invest in financial preparation, engage experienced advisors, and maintain transparent, well-organized records consistently survive due diligence with their valuations intact. The ones who do not often find themselves facing price reductions or deal conditions they could have avoided with better preparation.

Ready to take the next step? Contact FinLead today for a confidential discussion about your M&A goals.

Frequently Asked Questions

Q1: What is financial due diligence in M&A?

Financial due diligence is an independent review of a company's financial records conducted by the buyer before completing an acquisition. It verifies revenue quality, EBITDA accuracy, working capital, and any undisclosed financial risks.

Q2: What financial documents are needed for M&A due diligence?

Key documents include three years of audited financial statements, monthly management accounts, revenue schedules by client and contract, payroll records, bank statements, related-party transaction details, and working capital analysis.

Q3: What is EBITDA normalization in M&A?

EBITDA normalization adjusts reported earnings to remove one-time items, owner-specific costs, and non-recurring revenues to reflect the true, sustainable earnings power of the business. Buyers use normalized EBITDA as the basis for valuation.

Q4: What is working capital in an M&A transaction?

Working capital is the difference between current assets and current liabilities. In M&A, a target working capital is negotiated, and the deal price is adjusted up or down based on whether the actual working capital at closing is above or below the target.

Q5: What causes price reductions during due diligence?

Common causes include revenue quality issues, understated liabilities, undisclosed related-party transactions, tax exposures, contingent liabilities not reflected in accounts, and working capital deficiencies discovered during the financial review.

Q6: What is vendor due diligence?

Vendor due diligence is a financial review commissioned by the seller before entering the market. It proactively identifies issues buyers are likely to find and gives the seller time to address them, resulting in a smoother and faster buyer due diligence process.

Q7: How important are audited accounts in an M&A transaction?

Audited accounts are critical. Buyers place significantly less confidence in management accounts that have not been independently verified. Having audited financials for at least two years substantially increases buyer confidence and reduces due diligence complications.

Q8: What is a quality of earnings report?

A quality of earnings report, often called a QofE, is a financial due diligence deliverable prepared by the buyer's accountants. It assesses the sustainability and accuracy of reported earnings, including revenue quality, EBITDA normalization, and working capital analysis.

Explore FinLead's advisory services